Overview

In this blog post, I'm excited to share one of my earliest stock reports, focusing on Shopify (SHOP:NYSE) as of 11/03/2021. This report was a significant learning experience for me, providing a deep dive into the company's financials, business model, and growth potential. It also allowed me to compare Shopify's performance with its competitors and assess its position in the e-commerce industry.

Key Takeaways:

Company Overview: Shopify is a leading commerce platform that offers a range of tools and services for online businesses. Over the years, it has expanded its offerings and attracted even large-scale businesses to its platform.

Revenue Analysis: The report provides a detailed breakdown of Shopify's revenue, particularly focusing on its Subscription and MRR (Monthly Recurring Revenue) streams. I also analyzed their balance sheet and income statements, highlighting some of the accounting tricks that they potentially used.

Valuation: Based on growth rate analysis and PE ratios, the report provides a price target for Shopify and discusses its valuation in comparison to competitors.

Final Thoughts: While Shopify showcased immense growth potential, it's essential to consider the company's performance in regular market conditions and the impact of one-time gains on its earnings.

Reflection:

This early attempt at stock report writing was instrumental in shaping my understanding of company research and report creation. It taught me the importance of diving deep into financial statements, understanding industry trends, and making informed predictions based on data. As I share this with you, I hope it offers a glimpse into my journey of financial analysis and serves as an inspiration for budding analysts to dive deep and keep learning.

Company Overview

United Tractors, a subsidiary of PT Astra International Tbk ("Astra"), stands as a testament to Indonesia's industrial prowess. Astra, one of the largest and most established business groups in Indonesia, has a rich history of serving various industries and sectors with unparalleled expeortise. United Tractors has been publicly traded since September 19, 1989, when it listed its shares on the Indonesia Stock Exchange, which was formerly known as the Jakarta Stock Exchange and Surabaya Stock Exchange. Astra currently holds a majority stake in the company, owning 59.5% of its shares, while the rest are held by the public.

Diving deeper into its operations, United Tractors has strategically positioned itself as a dominant player across multiple sectors in Indonesia. The company's expansive portfolio is organized into six core business pillars:

Construction Machinery: United Tractors offers a range of construction machinery products and services, ensuring that clients have access to top-tier equipment and support for their projects.

Mining Contracting: With expertise in mining operations, the company provides comprehensive mining contracting services, ensuring efficient and sustainable extraction processes.

Coal Mining: United Tractors is actively involved in coal mining, contributing to Indonesia's energy sector and global coal supply.

Gold Mining: The company has also ventured into gold mining, tapping into the lucrative precious metals market.

Construction Industry: Beyond machinery and mining, United Tractors is also engaged in the broader construction industry, offering services and solutions for various infrastructure projects.

Energy: Recognizing the importance of sustainable energy, the company has diversified into the energy sector, aiming to provide cleaner and more efficient energy solutions.

In essence, United Tractors is not just a company; it's an institution that has been instrumental in shaping the industrial landscape of Indonesia. Through its diverse business ventures and unwavering commitment to excellence, the company continues to drive growth and innovation in the region.

Decoding the Numbers: Financial Insights

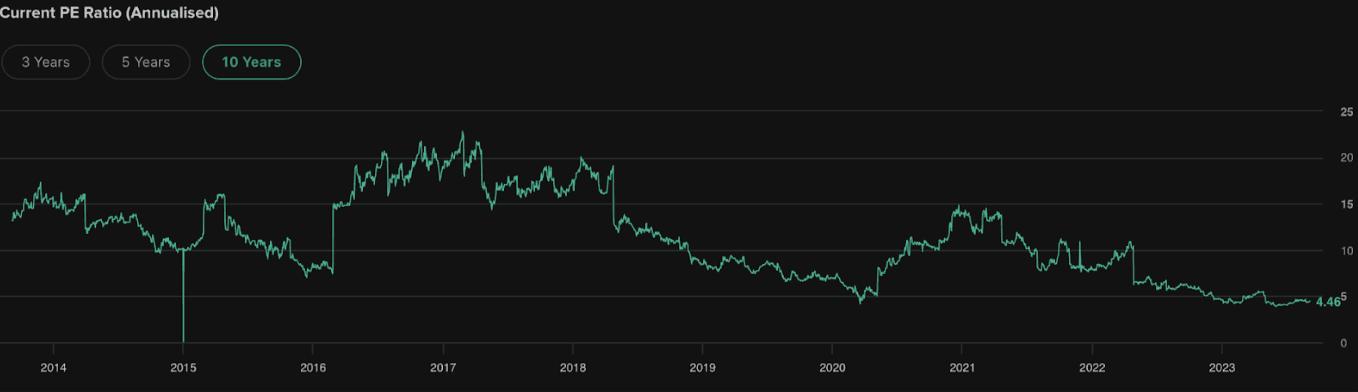

Price-to-Earnings (P/E) Ratio: 4.44

Analysis:

The Price-to-Earnings (P/E) ratio is a valuation metric that measures the price investors are willing to pay for each unit of earnings generated by a company. A P/E ratio of 4.44 for UNTR suggests that investors are currently paying Rp 4.44 for every Rp 1 of earnings the company generates. When compared to its peak P/E ratio of 22.81 in 2017, the current ratio indicates that the company's stock is significantly undervalued. This disparity between the past and present P/E ratios is an attractive proposition for investors, especially when considering that UNTR's operating profit margins are on the rise. While these margins may exhibit cyclical behavior, the overall growth trend in profitability, combined with a low P/E ratio, underscores the potential value proposition of UNTR as an investment.

Price-to-Book (P/B) Ratio: 1.39

Analysis:

Analysis:

The Price-to-Book Value (P/BV) ratio is a critical financial metric that gauges a company's market valuation relative to its book value. For UNTR, the P/BV ratio stands at a notable 1.39. When benchmarked against the sector average of 1.24, this ratio is higher, suggesting that the market values UNTR's net assets at a premium compared to its sector peers.

One significant factor that could justify this higher P/BV ratio is the company's market capitalization. UNTR’s market capitalization is 100,154 B, which is substantially larger than the sector average of 1,856 B.

In this scenario, the vast differential in market cap also implies that UNTR carry lower capital impairment risk. UNTR carry lower perceived risks for several reasons:

Diversification: UNTR has a diversified portfolio of products or services, reducing their reliance on a single revenue source and thereby decreasing business risk.

Financial Flexibility: A higher market capitalization often provides companies with better access to capital markets, allowing them to secure financing at more favorable terms.

Operational Resilience: UNTR can weather economic downturns more effectively due to their resources, established market presence, and ability to adapt to changing market conditions.

This perception of lower risk, combined with the factors mentioned earlier, can lead to a willingness among investors to pay a premium over the company's book value, resulting in a higher P/BV ratio.

Debt-to-Equity Ratio: 0.07

Current Ratio: 1.36

Return on Equity (ROE): 30.44%

Analysis:

Return on Equity (ROE) is a critical financial metric that measures a company's ability to generate profit from its shareholders' equity. An ROE of 30.44% indicates the company's efficiency in using shareholders' funds to produce earnings.

Growing Profitability: An increasing ROE indicates that UNTR’s net income is growing at a faster rate than its equity. Currently, the EPS YoY annual growth rate is 104.34%. This suggests that UNTR is effectively leveraging its resources to increase its earnings.

Competitive Advantage: UNTR's high and increasing ROE suggests a sustainable competitive advantage. Its effective business model and economies of scale make it well-positioned to generate profits. Rising ROE also signals higher returns on investment, making the stock more attractive and potentially leading to positive implications for its valuation and investor confidence.

Overall, it indicates that management is effectively deploying shareholders' capital, and the company is in a strong position to deliver value to its shareholders.

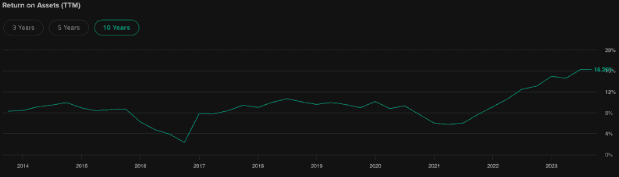

Return on Assets (ROA): 16.26%

Analysis:

Return on Assets (ROA) is a key financial metric that measures a company's ability to generate profit from its total assets. An ROA of 16.26% for UNTR indicates that the company is able to generate a profit of 16.26% for every unit of total assets.

When comparing UNTR's ROA of 16.26% to the sector average of 5.21%, several observations can be made:

Superior Asset Efficiency: UNTR's ROA is significantly higher than the sector average, suggesting that the company is more efficient in using its assets to generate profit than its peers.

Higher Profitability: A higher ROA typically indicates higher profitability. Given that UNTR's ROA is more than three times the sector average, it suggests that the company is not only generating higher profits but is also doing so more efficiently relative to its asset base.

This differential suggests that UNTR is operationally and strategically well-positioned within its sector, making it a standout performer in terms of asset efficiency and profitability.

Intrinsic Value Estimation:

Worst Case Scenario

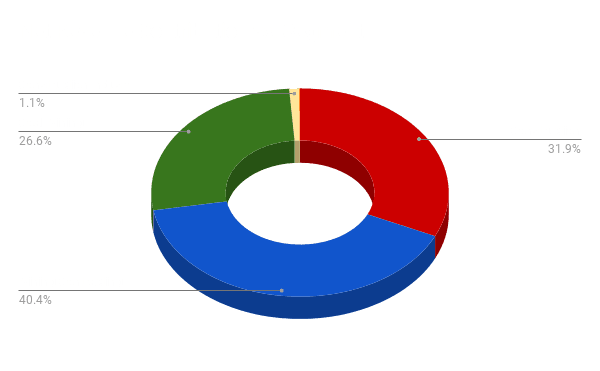

In evaluating the investment potential of UNTR, even under a pessimistic scenario where we project a declining growth rate due to decreasing coal prices—a significant concern given that coal mining constitutes 29% (as of Q2 2023) of their business operations—the numbers still present a compelling case. The intrinsic value of UNTR, based on the Discounted Cash Flow (DCF) analysis, stands at IDR63,301.15. This is significantly higher than its current enterprise value of IDR26,700.00. This discrepancy provides a substantial margin of safety of >50%, meaning that even if our assumptions and projections are off by half, the stock still offers value at its current price. Furthermore, it's crucial to note that while the coal segment faces challenges, UNTR's construction machinery arm, represented by Komatsu, remains a dominant force in the domestic market. They have consistently outperformed competitors such as Sany, Hitachi, and Caterpillar. This leadership position in a key segment of their business provides a buffer against the challenges faced in the coal sector. Thus, even in a worst-case scenario, UNTR's diversified operations and market leadership in construction machinery make it a worthy investment consideration, especially given the free cash flow and large margin of safety.